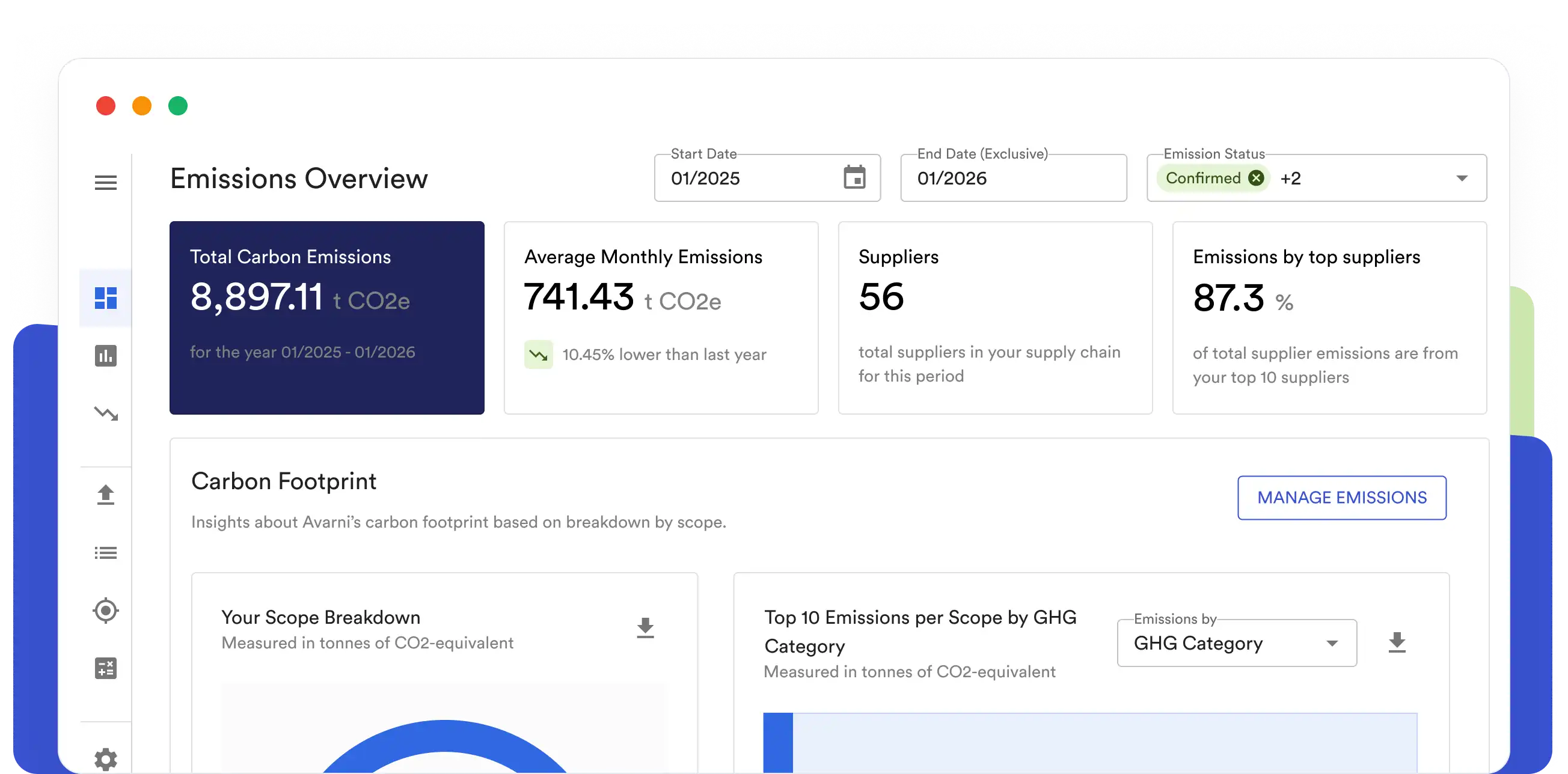

The introduction of the Australian Sustainability Reporting Standards (ASRS) marks a shift in how organisations approach emissions reporting. For Group 1 entities, Scope 3 puts pressure on existing processes, data quality, and internal ownership.

For CFOs and finance leaders, this is not just a sustainability exercise. Scope 3 reporting sits squarely within financial governance, audit readiness, and risk management. Getting ahead of the requirements early will determine how smooth the transition is over the next few reporting cycles.

What Group 1 needs to report and when

Group 1 reporters under the ASRS are the largest organisations, and the first to comply. While Scope 1 and Scope 2 disclosures come first, Scope 3 is phased in shortly after, with limited relief in the initial year.

The practical timing depends on your reporting cycle. For organisations reporting on a calendar year, the window to prepare for Scope 3 is shorter and requires action early in the reporting period. For those with a June year-end, there is slightly more time, but the preparation effort remains significant given the scale of data required.

In both cases, most organisations effectively have one reporting cycle to build a defensible Scope 3 inventory. That is a tight window given the complexity of value chain data, supplier engagement, and methodology decisions.

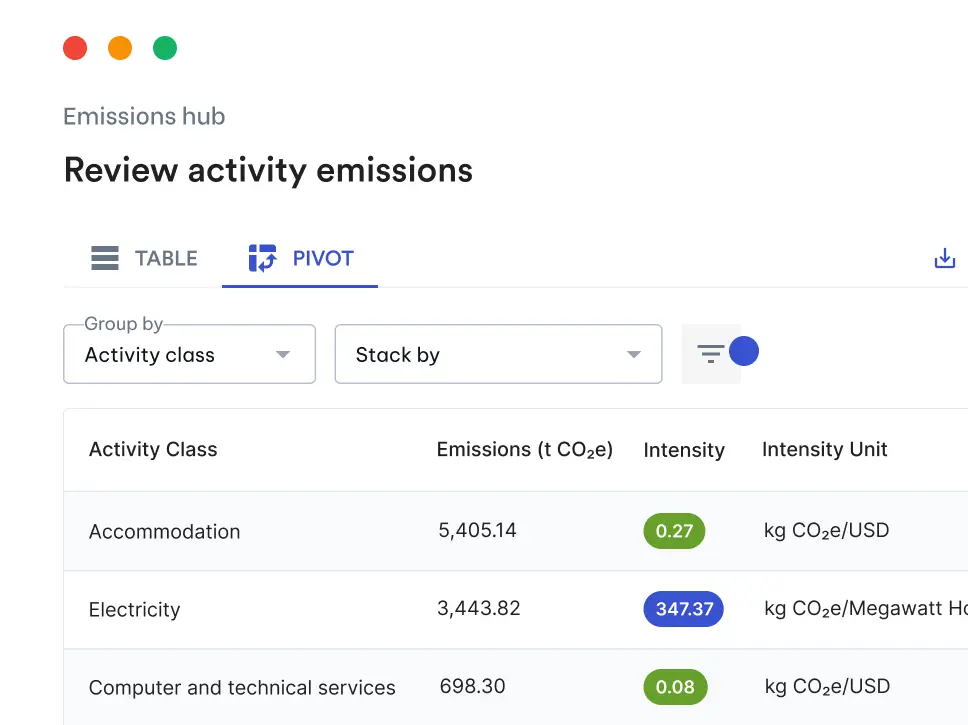

Scope 3 covers all indirect emissions across the value chain. For most organisations, this represents the majority of their total footprint. Categories like purchased goods and services, transport, and use of sold products can quickly outweigh operational emissions.

The challenge is building a defensible, auditable inventory that aligns with the GHG Protocol and can stand up to regulatory scrutiny.

Why Scope 3 is difficult in practice

Scope 3 is fundamentally different to Scope 1 and 2 because the data sits outside your organisation. You are relying on suppliers, partners, and internal systems that were never designed for emissions reporting.

Most finance teams encounter three immediate issues.

The first is fragmented data. Spend data sits in finance systems, logistics data sits elsewhere, and supplier information is often incomplete. Pulling this together into a single dataset is time consuming and error prone.

The second is methodology. There are multiple valid ways to calculate emissions, especially for Scope 3. The choice of emission factor database, calculation method, and level of detail can materially change the reported footprint.

The third is scale. Even a mid-sized organisation can have thousands of suppliers and transactions. Manually mapping these to emission factors is not sustainable, particularly under audit conditions.

Starting with a practical baseline

For Group 1 reporters, the priority is completeness and defensibility, not perfection.

The GHG Protocol allows for different calculation methods depending on data availability. In practice, most organisations start with the spend-based method for categories like purchased goods and services. This provides full coverage quickly and establishes a baseline.

The spend-based approach uses financial data and applies emission factors based on industry averages. While less precise than activity-based methods, it is widely accepted for initial reporting and enables organisations to identify material categories early.

From there, effort should be focused on the most material categories. Typically, a small number of categories will account for the majority of emissions. This is where finance teams should prioritise improving data quality and moving to more accurate methods over time.

The role of emission factors and data choices

Emission factors sit at the core of any Scope 3 inventory. The choice of database and factor has a direct impact on reported emissions and audit outcomes.

For Australian reporters, this often includes local databases such as the National Greenhouse Accounts (NGA) factors, AusLCI, and IELAB, particularly where activities occur domestically or where alignment with national guidance is expected. These can be complemented with global databases like EPA, BEIS, and EXIOBASE where there are gaps in coverage or where supply chains extend internationally.

Different databases offer different levels of granularity, geographic coverage, and unit types. For example, EPA provides highly detailed categories, while EXIOBASE offers broader global coverage. Both are valid, but the choice depends on the organisation’s data and reporting needs.

Consistency is critical. Once a methodology is chosen, it needs to be applied year on year to ensure comparability. Changes in methodology must be documented and justified, particularly as audits become more rigorous.

Finance teams should treat emission factors in the same way as accounting policies. They need governance, documentation, and clear ownership.

Moving beyond averages to supplier data

While spend-based methods are a practical starting point, ASRS reporting will increasingly push organisations towards higher quality data.

This means engaging suppliers and collecting primary data where possible. Supplier-specific emission factors provide a more accurate view of emissions and allow organisations to track real decarbonisation progress.

The process is not simple. It requires collecting activity data from suppliers, calculating their emissions, and converting that into usable factors. It also requires consistent methodology over time to ensure reported changes reflect actual performance, not calculation differences.

For CFOs, this introduces a new layer of supplier risk and dependency. Supplier engagement is no longer just a procurement function. It becomes part of financial reporting integrity.

Audit readiness and governance expectations

ASRS reporting brings Scope 3 into the same level of scrutiny as financial disclosures. This means documentation, controls, and audit trails are non-negotiable.

Every calculation needs to be traceable. This includes how data was sourced, which emission factors were used, and how assumptions were applied.

Manual processes, particularly spreadsheets, introduce significant risk at this stage. Errors in unit conversions, factor selection, or categorisation can lead to misstatements. These risks are already well understood in carbon accounting and often lead to rework or loss of confidence in reported numbers.

Establishing clear processes, ownership, and systems early will reduce the burden as reporting requirements expand.

What finance leaders should focus on now

The organisations that will handle Scope 3 well are the ones that treat it as a finance problem, not just a sustainability initiative.

This starts with aligning internal teams. Finance, procurement, and sustainability need to work together to define data flows, responsibilities, and reporting timelines.

It also requires investment in systems and processes that can scale. The volume of data and complexity involved in Scope 3 cannot be managed manually over the long term.

Finally, it requires a clear roadmap. Start with a complete baseline using available data. Identify material categories. Improve data quality where it matters most. And build towards supplier-specific data over time.

Summary

- Group 1 ASRS reporters need to disclose Scope 3 emissions shortly after initial reporting, leaving limited preparation time

- Scope 3 is complex due to fragmented data, multiple methodologies, and the scale of supplier and transaction data

- A spend-based approach is the most practical way to establish a complete baseline aligned with the GHG Protocol

- Emission factor selection and consistency are critical for audit-ready, defensible reporting

- Over time, organisations will need to shift towards supplier-specific data to improve accuracy and track decarbonisation

- Strong governance, documentation, and systems are essential as Scope 3 becomes subject to audit scrutiny

How Avarni can help

Scope 3 reporting under the ASRS is not just a one-off exercise. It is an ongoing process that requires consistent methodology, scalable data handling, and audit-ready outputs.

Avarni is built to handle exactly this.

It brings together the core components required to deliver a defensible Scope 3 inventory. This includes access to leading emission factor databases, automated mapping of business activity data to the right factors, and built-in workflows that prioritise the most material categories first.

For finance teams, this means less time spent managing spreadsheets and more confidence in the numbers being reported. Data is structured, calculations are consistent, and every output is backed by a clear audit trail.

As requirements evolve, Avarni also supports the transition from spend-based estimates to supplier-specific data. Supplier engagement workflows, data collection, and factor generation can all be managed in one place, helping organisations improve accuracy over time without rebuilding their process each year.

If you are preparing for Scope 3 under the ASRS, now is the time to put the right foundations in place.

Request a demo to see how Avarni can support your reporting requirements and reduce the complexity of Scope 3.