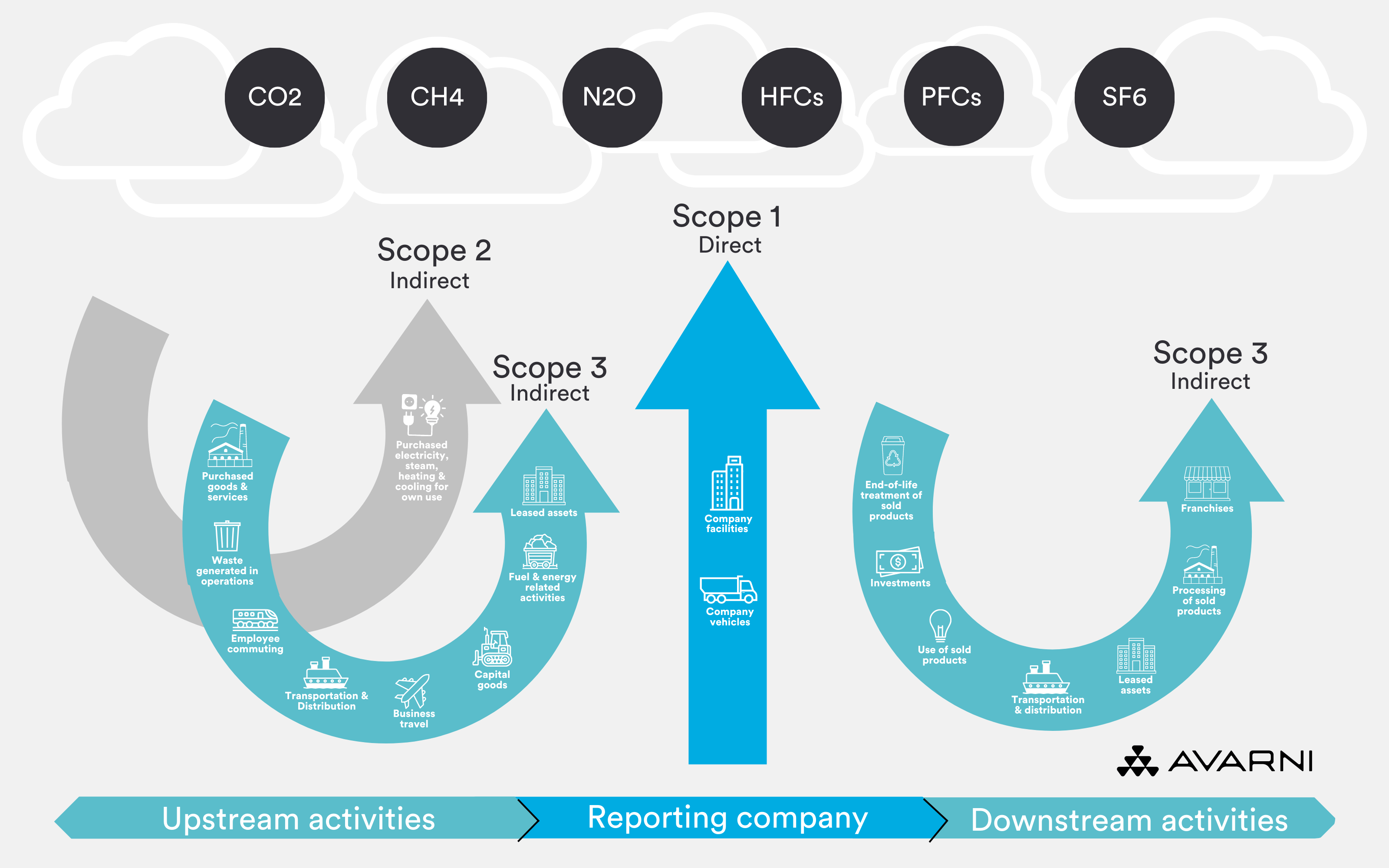

Within the GHG Protocol, there are three distinct “scopes” used to categorise direct and indirect greenhouse gas (GHG) emissions based on their proximity to — and degree of control by — the reporting organisation.

The GHG Protocol is a widely recognised framework for measuring and reporting greenhouse gas emissions. It is regarded as an international carbon accounting standard and forms the basis for frameworks such as TCFD, GRI, and CDP. The Protocol helps organisations measure emissions, set reduction targets, and report progress.

Scope 1: Direct emissions

Scope 1 covers direct emissions that are owned or controlled by the organisation. These emissions come from sources that the company operates and can be relatively straightforward to quantify and manage. Scope 1 emissions are typically divided into four categories:

- Stationary combustion

Fossil fuel combustion in stationary equipment such as boilers, furnaces, burners, turbines, heaters, incinerators, engines, flares, etc. These are used for heating, cooling, and industrial processes.

- Mobile combustion

Emissions from transportation vehicles operated by the organisation, including aircraft, automobiles, trucks, boats, ships, barges, and other vessels. (An increasing share of transport emissions may shift to Scope 2 where electricity for electric vehicles is purchased from an external provider.)

- Fugitive emissions

Intentional or unintentional releases from leaks and other irregular emissions of gases or vapours from pressure-containing equipment, such as refrigerant leaks.

- Process emissions

Emissions from chemical reactions in industrial processes and on-site manufacturing.

Note: Certain emissions (for example CO2 from biomass combustion or some gases outside the scope of the Kyoto Protocol such as CFCs and NOx with specific reporting rules) may be reported separately and not included in Scope 1 totals.

Scope 2: Indirect emissions (energy)

Scope 2 includes indirect emissions associated with the consumption of purchased energy by the organisation — for example, purchased electricity, heat, steam, and cooling. These emissions physically occur at the site where the energy is generated but result from the organisation’s energy use.

Scope 3: Other indirect emissions (value chain)

Scope 3 encompasses all other indirect emissions that occur in an organisation’s value chain — emissions the organisation has influence over but does not directly control. Scope 3 is comprehensive and covers cradle-to-grave emissions from upstream suppliers through downstream customers. These emissions are typically the largest portion of an organisation’s carbon footprint but are the most challenging to measure.

Scope 3 is divided into 15 categories. These are commonly grouped into upstream (before the organisation’s operations) and downstream (after the organisation’s operations) activities.

Upstream categories

1. Purchased goods and services — Cradle-to-gate emissions from the production of goods and services purchased by the company in the reporting year.

2. Capital goods — Emissions from the production of capital goods used by the company (buildings, machinery, vehicles, etc.).

3. Fuel- and energy-related activities (not included in Scope 1 or 2) — Emissions related to extraction, production, and transportation of fuels and energy purchased and consumed by the company.

4. Upstream transportation and distribution — Transport and distribution of inputs (raw materials, products) from suppliers to the company’s facilities, including third-party warehousing.

5. Waste generated in operations — Emissions from disposal and treatment of waste generated by company operations (e.g., methane (CH4) and nitrous oxide (N2O) from landfilling).

6. Business travel — Emissions from employee business travel (air travel, trains, taxis, rental cars, etc.).

7. Employee commuting — Emissions from employees commuting to and from work (cars, public transport, cycling, etc.).

8. Upstream leased assets — Emissions from leased assets (buildings, equipment) that the company leases and that are not already included in Scope 1 or 2.

Downstream categories

9. Downstream transportation and distribution — Transport and distribution of sold products in vehicles and facilities not owned or controlled by the company.

10. Processing of sold products — Emissions from further processing of intermediate products sold by the company (by third parties).

11. Use of sold products — Emissions from the use, operation, maintenance, and repair of sold products by end users.

12. End-of-life treatment of sold products — Emissions from disposal or recycling of products sold by the company (often difficult to measure due to consumer behaviour).

13. Downstream leased assets — Emissions from the operation of assets owned by the reporting company and leased to other entities (not already in Scope 1 or 2).

14. Franchises — Emissions from franchisees’ operations (where applicable and not included in Scope 1 or 2).

15. Investments — Emissions associated with investments (relevant for investors and financial institutions: equity investments, debt investments, project finance, managed assets, client services, etc.).

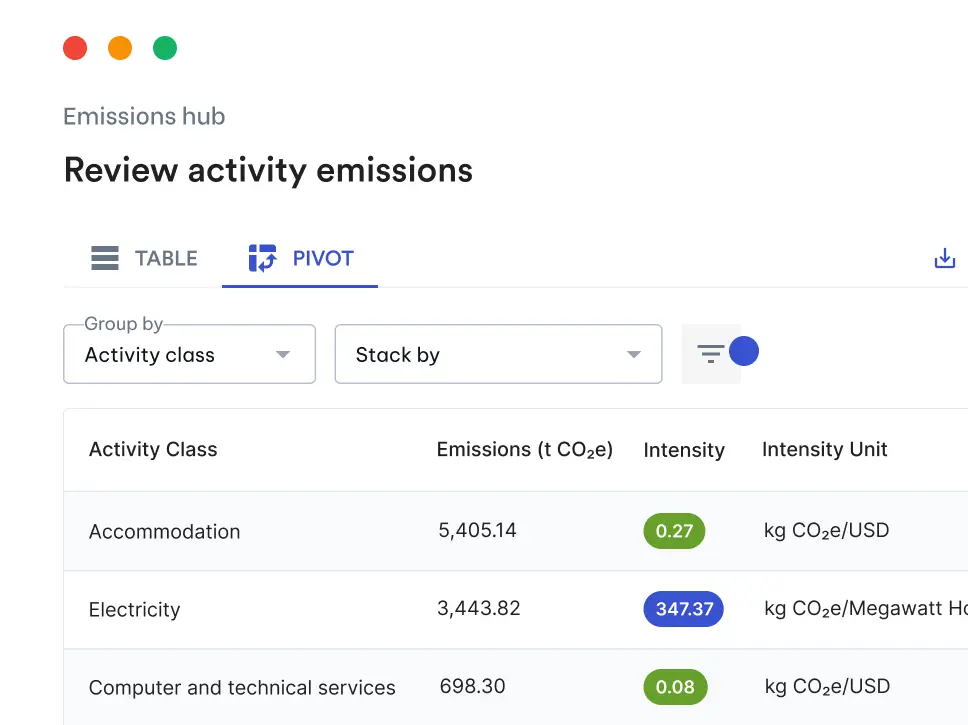

Calculating Scope 3 requires collecting data from suppliers, customers, and other value-chain partners, making it time-consuming and complex. However, it is often essential for understanding the full climate impact of an organisation.

Why measure Scope 1, 2, and 3?

Measuring all three scopes enables organisations to:

- Understand the full environmental impact of their operations and value chain.

- Identify and prioritise reduction opportunities across direct operations and the value chain.

- Comply with emerging regulatory and investor disclosure requirements (for example, EU carbon pricing and reporting regimes, proposed SEC climate-related disclosure rules, and national requirements such as in New Zealand).

- Demonstrate leadership on sustainability and maintain competitive advantage as stakeholders increasingly demand transparency.

How Avarni can help

Measuring and reducing carbon emissions can enhance a company’s value chain and support a more sustainable future. Avarni facilitates this by:

- Making it easy to import spend and activity data.

- Visualising your organisation’s Scope 1, 2, and 3 emissions.

- Using a comprehensive methodology to identify all 15 Scope 3 categories and collect data from your supply chain.

- Enabling forecasting of future emissions with scenario modelling for supply chain changes over time.

- Factoring in external macroeconomic variables when modelling emissions scenarios.

- Allowing modelling of financial costs under different scenarios by setting carbon prices.

- Providing an effective solution to measure, track, and reduce Scope 1–3 emissions.

Get in touch with us to learn how Avarni can support your decarbonisation journey.