Across hundreds of conversations we’ve had at Avarni with CFOs and finance leaders in Australian organisations, one theme is consistent: carbon reporting now sits within controlled reporting processes alongside financial disclosures. As assurance requirements tighten under AASB S2, finance teams are strengthening systems, documentation and internal controls so emissions data can withstand the same scrutiny as financial data.

This article focuses on the mechanics of that shift. For finance teams responsible for delivering compliant disclosures, supporting assurance and reducing reporting risk, the priority is building infrastructure that is scalable, traceable and aligned with existing finance architecture.

Step one: stabilise Scope 1 and Scope 2 data flows

Before expanding into more complex areas, leading organisations are stabilising their core data flows.

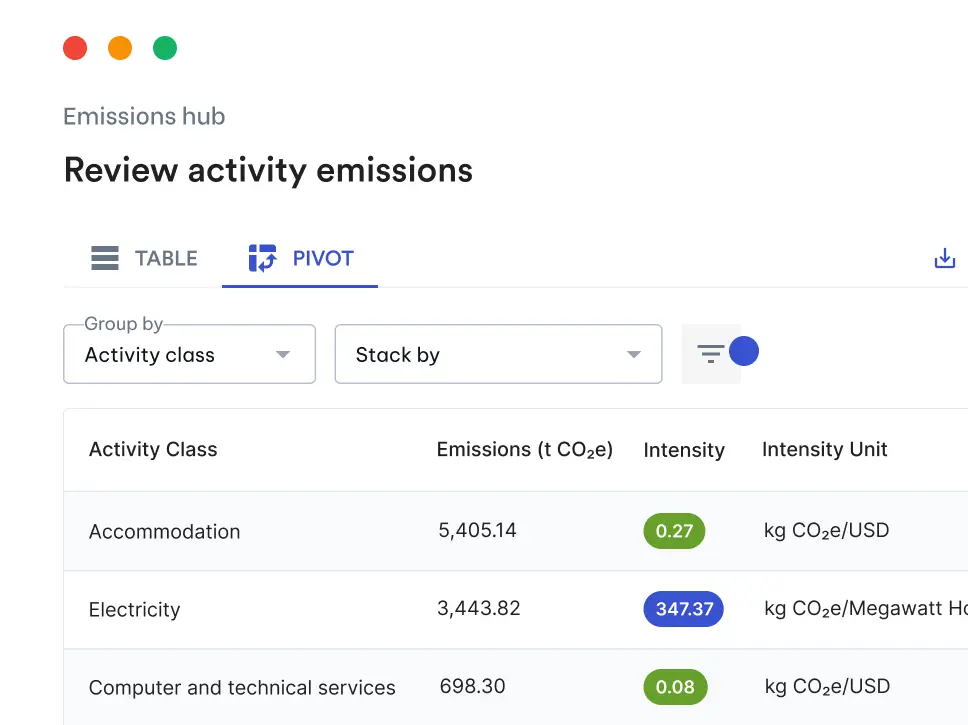

Scope 1 and Scope 2 calculations are generally straightforward from a technical perspective, however process design often introduces risk. Energy invoices arrive in PDFs, fuel data sits across multiple portals, refrigerants are logged manually and consolidation frequently occurs in Excel at quarter end. This creates reliance on individual workbooks and informal controls.

The first stage of maturity is automation and centralisation. Organisations are automating invoice ingestion from energy retailers and fuel providers, standardising site and meter identifiers, maintaining emission factors within a controlled library and implementing a calculation layer that records inputs, factors and outputs in a structured way.

The focus is on control, traceability and repeatability across the reporting workflow. Finance teams expect every emissions number to be traceable to a source document and reproducible without relying on undocumented spreadsheet logic. Once Scope 1 and Scope 2 data flows are automated and auditable, the organisation has a stable reporting base that can support further expansion.

Step two: anchor Scope 3 in the general ledger

Scope 3 Category 1 is where complexity increases. Transaction volumes are large and supplier data quality varies significantly, which often leads to hesitation or delays.

More advanced finance teams begin with the general ledger because it provides completeness and alignment with existing controls. The GL captures the full population of spend, is already audited and integrates directly with financial reporting structures. Using it as the foundation for spend-based emissions creates an immediate baseline that is defensible under assurance.

A structured workflow typically involves extracting full-year spend by account from the ERP, mapping accounts to Scope 3 categories, applying a consistent emission factor database and documenting mapping logic and assumptions. This approach ensures emissions totals can be reconciled directly to audited spend, which materially reduces assurance risk.

The initial baseline establishes coverage and traceability, forming a stable foundation that can be progressively refined as data quality improves.

Step three: refine material categories methodically

Attempting to implement detailed activity-based or supplier-specific data across all categories in the first reporting cycle can introduce unnecessary complexity and execution risk.

A staged refinement approach provides stronger outcomes. Once a spend-based baseline is complete, finance teams identify material categories, which typically represent the majority of total emissions. These categories become the focus for improved data quality.

Material accounts can transition to activity-based calculations where reliable operational data exists. Supplier-specific emission factors can be introduced selectively for strategic suppliers where engagement is commercially practical. Throughout this process, core mapping logic remains stable to preserve comparability between reporting periods and maintain methodological integrity.

This structure allows reporting accuracy to improve over time while maintaining consistency and audit defensibility.

Step four: centralise emissions data to support multiple reporting requirements

Finance teams rarely manage a single disclosure framework. In addition to AASB S2, many organisations manage NGERS, NPI, board reporting requirements and customer data requests.

Operational burden increases significantly when each output is prepared independently.

A more efficient approach centralises emissions data within a single controlled environment where it is tagged by entity and facility, attributed to Scope categories, linked to financial accounts and supported by a documented basis of preparation. From this central dataset, regulatory reports, board packs and customer disclosures can be generated consistently.

Centralisation reduces duplication, improves consistency across disclosures and limits the reconciliation effort required each reporting cycle.

Step five: integrate with existing finance architecture

Strengthening carbon reporting infrastructure does not require a full-scale technology transformation. Organisations progressing efficiently are integrating carbon accounting into their existing finance and reporting ecosystems.

This typically involves file-based uploads or API feeds from ERP systems, integration with data lakes such as Snowflake and compatibility with established reporting tools including Power BI. Carbon data becomes another governed dataset within the broader finance environment and aligns with established reporting cycles and control frameworks.

An integration-focused approach keeps implementation timelines proportionate, reduces internal disruption and improves adoption within finance teams.

What finance-grade carbon reporting looks like

When finance leaders describe success, their measures are practical and control-focused. They expect to trace emissions numbers to source documentation, reconcile Scope 3 totals to audited spend, respond confidently to assurance queries and reduce manual handling across reporting cycles. They also require board-ready outputs to be produced efficiently and consistently.

Finance-grade carbon accounting is characterised by reliability, documentation and repeatability. Emissions data is embedded within existing reporting controls and governed with the same discipline applied to financial information.

Building reporting infrastructure that scales

Carbon reporting now functions as an ongoing reporting responsibility within finance. Systems and controls therefore need to support long-term scalability rather than short-term project delivery.

Organisations that stabilise data flows, anchor Scope 3 in the general ledger, refine methodology progressively, centralise reporting outputs and integrate with existing finance systems are establishing reporting infrastructure capable of evolving with regulatory expectations.

The result is a controlled and scalable reporting framework that reduces risk and supports confident disclosure.

Summary

- Stabilise and automate Scope 1 and Scope 2 data flows to establish a controlled reporting foundation.

- Use the general ledger as the basis for a complete and auditable Scope 3 baseline.

- Refine material categories progressively while maintaining consistent methodology.

- Centralise emissions data so multiple reporting frameworks draw from a single governed dataset.

- Integrate carbon accounting into existing ERP and BI architecture to minimise disruption.

- Finance-grade carbon reporting is defined by traceability, reconciliation and repeatability.