With the Australian Sustainability Reporting Standards (ASRS) now in effect, construction companies face growing pressure to disclose carbon emissions across their entire value chain. The sector has long focused on operational emissions from fuel and electricity use, but the bigger task is accounting for Scope 3 emissions, particularly embedded carbon in materials like steel, concrete and glass.

Construction is one of the most emissions-intensive industries globally, and governments, investors and clients are pushing for greater transparency. For firms bidding on infrastructure projects, commercial builds or government tenders, carbon reporting is becoming central to winning work and staying compliant.

Key takeaways

- ASRS (AASB S2) requires construction companies to disclose Scope 3 emissions, including embodied carbon in materials such as steel, concrete and glass.

- Embodied carbon made up 16% of Australia's built environment emissions in 2019, and is projected to reach 85% by 2050 without intervention as operational emissions fall.

- Government agencies and large developers are building embodied carbon requirements into procurement and tender processes.

- Firms that can quantify and reduce Scope 3 emissions gain an edge in tenders and better access to sustainability-linked finance.

Why Scope 3 is rising to the top

For most construction firms, Scope 1 and 2 emissions (fuel burned on-site, electricity use, owned vehicles) are a small share of the total footprint. The bulk sits in Scope 3: materials purchased, services subcontracted, and upstream supply chain activity.

Embodied carbon made up 16% of Australia's built environment emissions in 2019. Without intervention, the Green Building Council of Australia (GBCA) projects this will climb to 85% by 2050, as operational emissions fall with grid decarbonisation. For new high-performance buildings, embodied carbon already makes up around 45% of whole-of-life emissions.

The materials driving this are well known:

- Steel

- Cement and concrete

- Aluminium

- Glass

These emissions occur during manufacturing and transport, before materials reach the site. Many construction companies can't map them accurately yet, because the data sits across supplier tiers, inconsistent formats and procurement systems that weren't built with carbon in mind.

Projects targeting carbon neutrality or Green Star certification need to account for embodied carbon alongside operational emissions.

Regulations and reporting are moving fast

ASRS (AASB S2), aligned to the ISSB's IFRS S2, requires construction firms operating in or servicing the Australian market to disclose climate-related risks, including Scope 3 emissions. These disclosures need to be robust, auditable and grounded in data.

Government agencies and large developers are already embedding emissions requirements into procurement, expecting contractors and suppliers to quantify embodied carbon and show emissions reduction strategies. This will accelerate as regulators and clients demand more accountability across the project lifecycle.

Firms that ignore these shifts risk being excluded from tenders, or exposed to reputational and financial risk if their reporting doesn't hold up.

Opportunities beyond compliance

Construction companies that can track and reduce embodied emissions win more work, particularly in green buildings, infrastructure and government-funded projects.

Better carbon data also opens up sustainability-linked finance. Lenders and investors increasingly offer better terms to companies that can show credible decarbonisation strategies backed by real data. This matters most for vertically integrated construction firms with property development arms, or those in public-private infrastructure partnerships.

Understanding emissions at the material and project level helps construction firms make better decisions: choosing lower-carbon alternatives, working with sustainable suppliers, and avoiding design choices that lock in long-term emissions. This turns sustainability reporting into a source of commercial advantage rather than a compliance cost.

How construction firms can get started

The first step is visibility. Many construction companies still rely on spreadsheets, outdated emission factors, or incomplete supplier data, which leads to gaps and low confidence in the numbers.

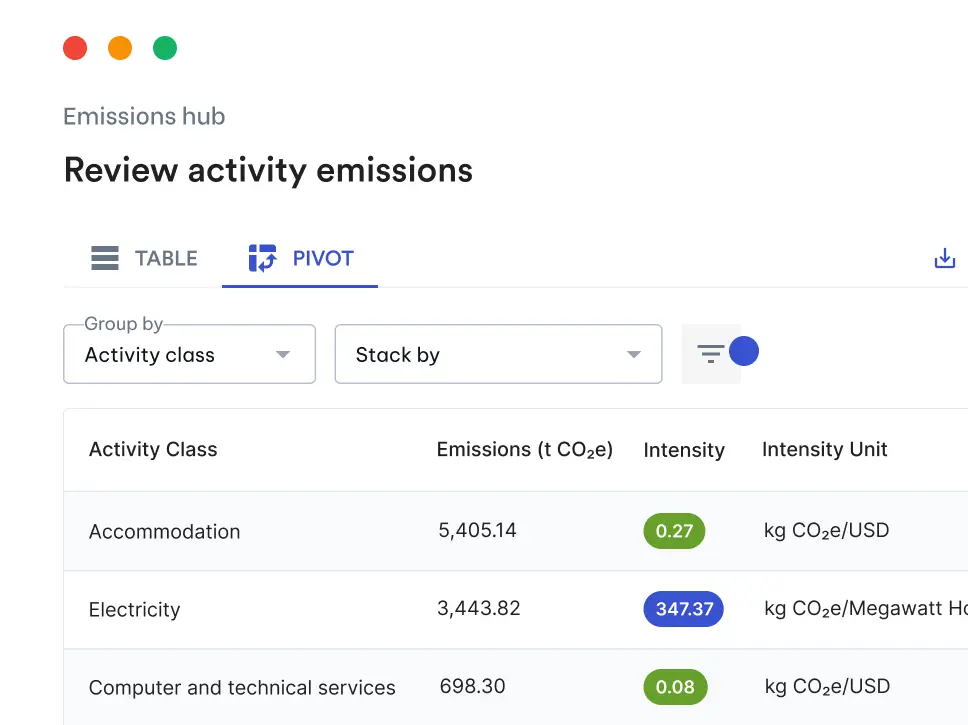

Avarni's construction industry tools streamline Scope 3 data collection across suppliers and spend categories. By using machine learning to map procurement data against emission factors, Avarni shows construction companies where their biggest emissions sit, including embedded carbon in purchased materials and subcontracted services.

This makes it easier to prioritise action, whether that means engaging key suppliers, switching materials, or setting data-backed reduction targets across projects, while keeping disclosures audit-ready.

Frequently asked questions

What is embodied carbon in construction?

Embodied carbon is the greenhouse gas emissions released during the manufacturing, transport and installation of building materials, such as steel, concrete, aluminium and glass, before a project is even operational.

Does ASRS apply to construction and infrastructure companies?

Yes. ASRS (AASB S2) applies to large construction and infrastructure companies that meet the relevant reporting thresholds under the Corporations Act, requiring disclosure of climate-related risks including Scope 3 emissions.

Which Scope 3 category covers embodied carbon in materials?

Embodied carbon in purchased construction materials typically falls under Scope 3, Category 1 (purchased goods and services) of the GHG Protocol, with subcontracted work often reported under the same category.

How can construction firms start measuring Scope 3 emissions?

Firms typically start by mapping procurement and supplier spend data against emission factors, then improving data quality over time by engaging key suppliers for primary data instead of relying on spend-based estimates alone.

Summary

- Why Scope 3 is rising to the top: Most construction emissions sit in Scope 3, particularly embodied carbon in materials like steel and concrete. GBCA data shows this could reach 85% of built environment emissions by 2050 without intervention.

- Regulations and reporting are moving fast: ASRS (AASB S2), aligned with ISSB's IFRS S2, requires disclosure of Scope 3 emissions, and procurement processes are already being rebuilt around embodied carbon requirements.

- Opportunities beyond compliance: Firms that track and reduce embodied emissions win more tenders and gain better access to sustainability-linked finance.

- How construction firms can get started: Visibility is the first step. Avarni helps construction firms map Scope 3 emissions across suppliers and materials, and turn that data into audit-ready disclosures.

- Frequently asked questions: Embodied carbon covers emissions from materials manufacturing and transport, sits under GHG Protocol Scope 3 Category 1, applies to construction and infrastructure companies under ASRS, and is best measured by mapping supplier and spend data against emission factors.

By treating embodied carbon as a design and procurement variable rather than just a disclosure line item, construction firms can turn ASRS compliance into a genuine competitive edge.

Originally published: 11/23/2025